filmov

tv

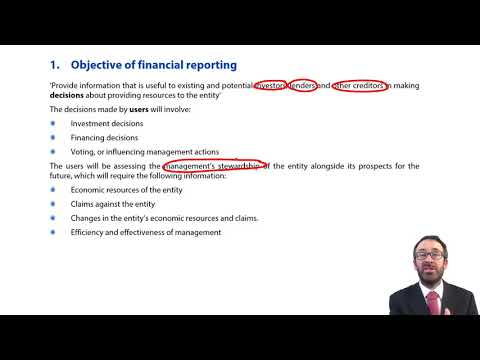

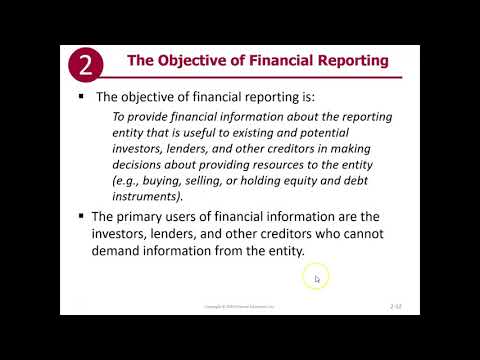

Objectives of Financial Reporting

Показать описание

After giving a brief overview of the learning objectives of the chapter, the measurement focus is outlined (including the difference between operational and fiscal accountability). The modified accrual basis of accounting and accrual basis of accounting are also compared and contrasted. Following that, the primary activities of the government are discussed as well as the two basic sets of financial statements involved (government-wide and fund financial statements). Funds are also defined, as well as the different categories of funds (governmental funds, proprietary funds, and fiduciary funds) - however, governmental funds are focused on the most during this lecture. Lastly, the dual effect of capital and related transactions is explained (including in-depth journal entries).

To receive additional updates regarding our library please subscribe to our mailing list using the following link:

0:06:17

0:06:17

0:06:40

0:06:40

0:01:08

0:01:08

0:05:52

0:05:52

0:01:51

0:01:51

0:08:36

0:08:36

0:19:09

0:19:09

0:07:30

0:07:30

3:01:09

3:01:09

0:12:04

0:12:04

0:02:18

0:02:18

0:07:42

0:07:42

0:01:07

0:01:07

0:02:19

0:02:19

0:15:27

0:15:27

0:03:00

0:03:00

0:02:40

0:02:40

0:06:38

0:06:38

0:13:14

0:13:14

0:03:07

0:03:07

0:01:20

0:01:20

0:12:11

0:12:11

0:00:31

0:00:31

0:04:30

0:04:30