filmov

tv

Moving Average Process - Applied Time Series Analysis in Python and TensorFlow

Показать описание

👉 Get the course at 87% off:

-----------------------------------

Let’s cover the moving average model.

The moving average model is used for forecasting. It uses the past forecast errors to predict the next point in time. We refer to the moving average model as the MA(q) model, where q is the order.

Here, we see a simulation of a moving average process of order 2. We will do the same in Python

Then, we plot the ACF function. What do you notice? It seems that after lag 2, the autocorrelation is not significant anymore.

Now you know that we can use the ACF plot to estimate the order q of a moving average model! After lag q, the autocorrelation should not be significant anymore. Alright, now let’s run some simulations in Python and see this for ourselves!

-----------------------------------

Let’s cover the moving average model.

The moving average model is used for forecasting. It uses the past forecast errors to predict the next point in time. We refer to the moving average model as the MA(q) model, where q is the order.

Here, we see a simulation of a moving average process of order 2. We will do the same in Python

Then, we plot the ACF function. What do you notice? It seems that after lag 2, the autocorrelation is not significant anymore.

Now you know that we can use the ACF plot to estimate the order q of a moving average model! After lag q, the autocorrelation should not be significant anymore. Alright, now let’s run some simulations in Python and see this for ourselves!

0:10:24

0:10:24

Moving Average Process - Applied Time Series Analysis in Python and TensorFlow

0:08:16

0:08:16

Advanced Statistics - Week 5 - Moving average process MA(q)

0:09:07

0:09:07

Moving Average (MA) Time Series Model

0:04:08

0:04:08

Example for Moving Average processes

0:10:42

0:10:42

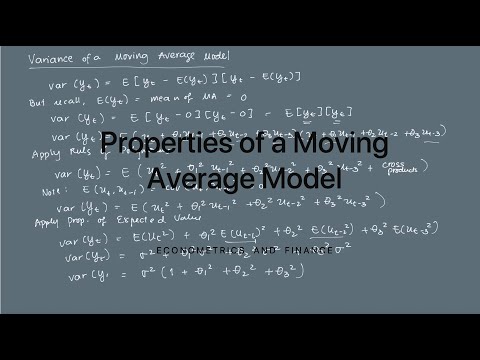

Properties of a Moving Average Model

0:15:45

0:15:45

Time Series Analysis | Auto regressive Process | Moving Average Process | AR(p) | MA(q) | ARMA Model

0:10:43

0:10:43

Auto-regressive and Moving Average models: AR(p) + MA(q)

0:16:15

0:16:15

Moving average model for time series econometrics (Excel)

0:44:59

0:44:59

Never Miss A Big Move With This Strategy

0:06:38

0:06:38

What is Moving Average? 📈 [Explained]

1:16:19

1:16:19

8. Time Series Analysis I

0:14:02

0:14:02

AR and MA models in EViews

0:07:08

0:07:08

Moving Average processes - Stationary and Weakly Dependent

0:09:26

0:09:26

Time Series Talk : ARIMA Model

1:01:36

1:01:36

What are moving average processes, Invertibility ?|Class 45,CS2-Risk Modelling & Survival Analys...

0:05:30

0:05:30

'Moving Averages' from Time Series in Statistics

0:04:52

0:04:52

Forecasting: Moving Averages, MAD, MSE, MAPE

0:03:47

0:03:47

Conducting a Moving Average in R

1:21:16

1:21:16

ES544 Random Processes | Some Examples | Random Harmonics & Moving Average Process

0:05:00

0:05:00

Forecasting: Weighted Moving Averages, MAD

0:03:23

0:03:23

Introduction to the Autoregressive Model

0:14:34

0:14:34

02417 Lecture 5 part C: ARMA models

0:30:01

0:30:01

The Best Ways to Use Moving Averages | Rick Bensignor

0:20:38

0:20:38

How to build ARIMA models in Python for time series forecasting

Комментарии