filmov

tv

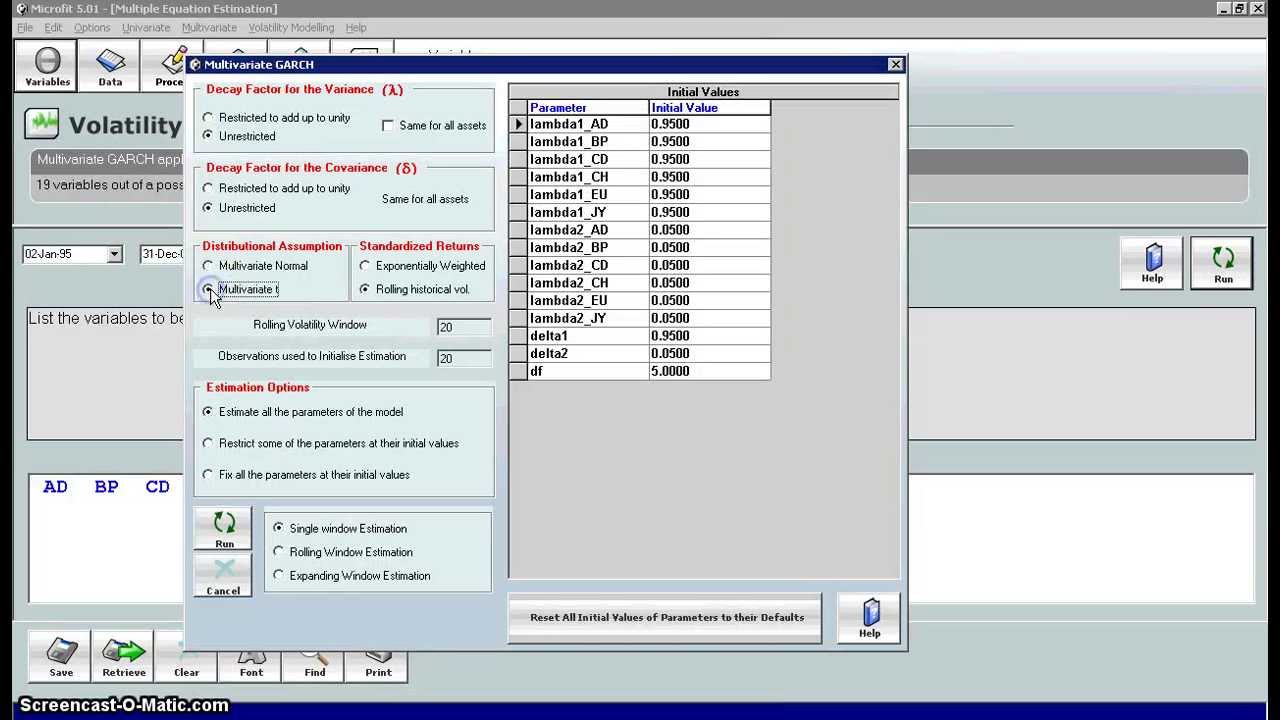

Advanced Econometrics using Microfit 5: MGARCH-DCC

Показать описание

Multivariate GARCH models are considered as one of the most useful tools for analyzing and forecasting the volatility of time series when volatility fluctuates over time. This feature demonstrates its availability in modeling the co-movement of multivariate time series with varying conditional covariance matrix.

0:08:41

0:08:41

0:03:21

0:03:21

0:02:39

0:02:39

0:11:22

0:11:22

0:02:34

0:02:34

0:12:41

0:12:41

0:09:40

0:09:40

0:16:38

0:16:38

0:02:06

0:02:06

0:00:40

0:00:40

0:00:34

0:00:34

0:05:58

0:05:58

0:04:37

0:04:37

0:11:06

0:11:06

0:02:23

0:02:23

0:10:47

0:10:47

0:01:59

0:01:59

0:00:11

0:00:11

0:00:52

0:00:52

0:22:16

0:22:16

0:05:17

0:05:17

0:02:17

0:02:17

0:05:30

0:05:30

0:01:02

0:01:02