filmov

tv

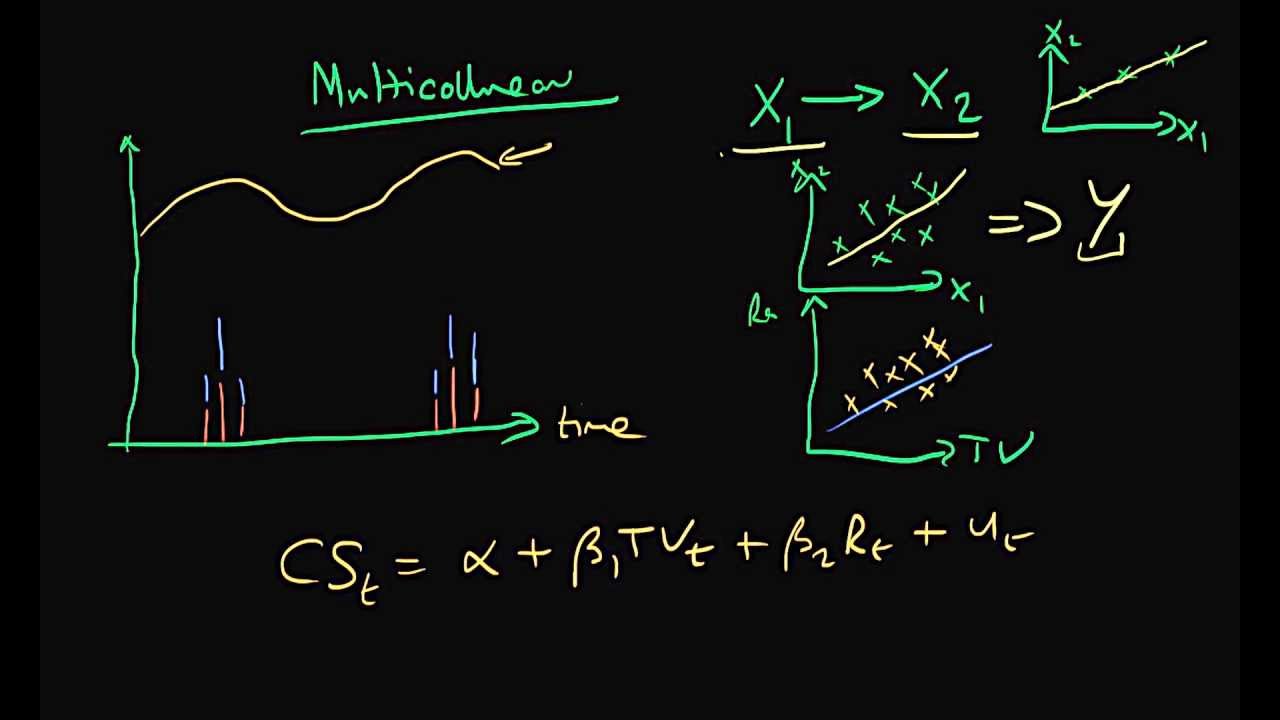

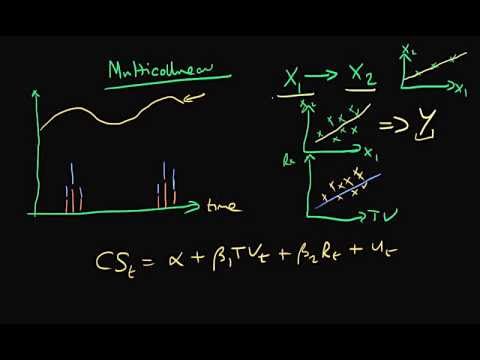

Multicollinearity

Показать описание

0:05:17

0:05:17

Multicollinearity

0:05:57

0:05:57

Multicollinearity (in Regression Analysis)

0:27:02

0:27:02

What is Multicollinearity? Extensive video + simulation!

0:05:05

0:05:05

Multicollinearity - Explained Simply (part 1)

0:21:01

0:21:01

Multicollinearity

0:05:28

0:05:28

Variance Inflation Factors: testing for multicollinearity

0:07:26

0:07:26

2.2.11 An Introduction to Linear Regression - Video 6: Correlation and Multicollinearity

0:10:46

0:10:46

Why multicollinearity is a problem | Why is multicollinearity bad | What is multicollinearity

0:10:55

0:10:55

Do we assume multicollinearity? No!

0:11:27

0:11:27

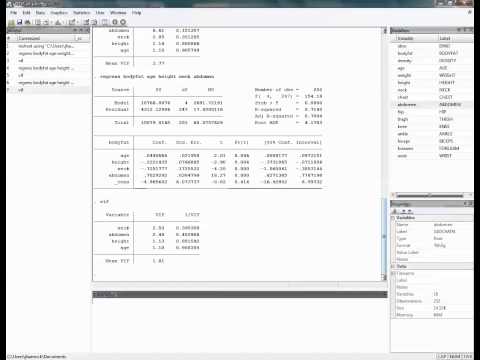

Understanding and Identifying Multicollinearity in Regression using SPSS

0:09:20

0:09:20

Multicollinearity (Playlist 1)

0:02:42

0:02:42

Multicollinearity in SPSS

0:17:33

0:17:33

Understanding Multicollinearity

0:28:30

0:28:30

Econometrics - Multicollinearity

0:05:29

0:05:29

Data Science Interview Questions- Multicollinearity In Linear And Logistic Regression

0:18:01

0:18:01

Multicollinearity and VIF (theory + R code)

0:02:58

0:02:58

Multicollinearity in SPSS

0:05:08

0:05:08

Multicollinearity | Heteroscedasticity | Autocorrelation | Ecoholics

0:45:53

0:45:53

Multicollinearity 1

0:08:08

0:08:08

Computing Multicollinearity Diagnostics in Stata

0:06:28

0:06:28

Multicollinearity and its detection methods

0:17:51

0:17:51

Lecture47 (Data2Decision) Multicollinearity

0:04:07

0:04:07

How Do You Handle Multicollinearity In Machine Learning-Asked In Interview

0:10:45

0:10:45

Variance Inflation Factor Simplified | Variance Inflation Factor in Multicollinearity | VIF

Комментарии