filmov

tv

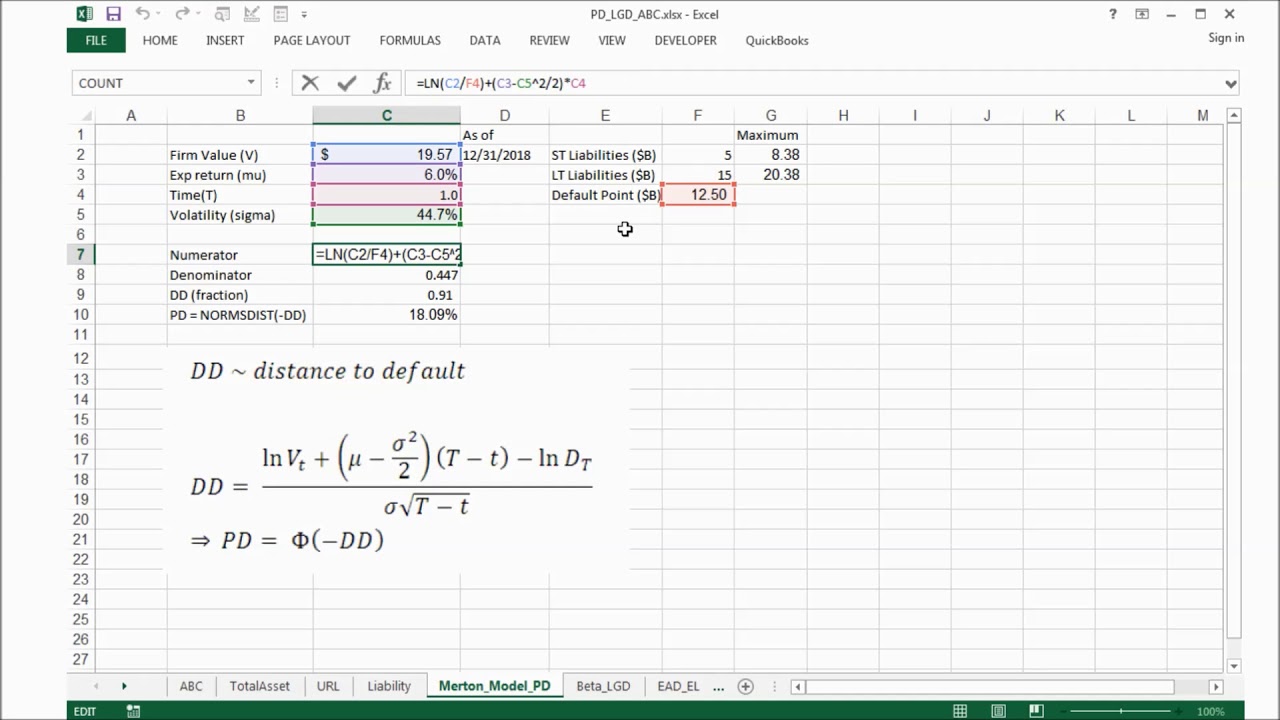

EAD, PD and LGD Modeling for EL Estimation

Показать описание

Calculated expected loss with actual financial data by modeling exposure at default, probability at default and loss given default.

0:04:13

0:04:13

3. Expected loss EL and its components PD LGD and EAD

0:16:47

0:16:47

EAD, PD and LGD Modeling for EL Estimation

0:06:10

0:06:10

Probability of Default (PD) and Loss Given Default (LGD) Explained

0:08:21

0:08:21

The Use of Loss Given Default (LGD) - Deloitte

0:24:52

0:24:52

Monitoring and Backtesting Credit Risk Models || PD, LGD, EAD || Basel || Risk Management

0:13:59

0:13:59

ECL Calculation Simplified / Practical Approach / IFRS 9

1:03:29

1:03:29

CREDIT RISK MODELLING - Scorecards | IFRS 9 | Basel | Stress Testing | Model Validation

0:02:46

0:02:46

Expected Credit Loss: Basel III vs IFRS 9

0:00:25

0:00:25

Credit Risk Analytics Study Pack: PD, LGD, EAD, Application Scorecard, Risk Model Validation

0:00:50

0:00:50

Stages in Probability of Default(PD) Model Development| Credit Risk Analytics(PD, LGD, EAD)

0:02:16

0:02:16

Steps in Probability of Default Model Development|Credit Risk Analytics- PD, LGD, EAD

0:26:26

0:26:26

Point in LGD using Jacob Frye Approach | IFRS 9 | ECL | Credit risk modelling

0:51:29

0:51:29

Credit Risk Modeling (For more information, see www.bluecourses.com )

0:47:04

0:47:04

Credit Risk Modelling PD LGD Introduction to BSM and ASRF Framework Day07

1:10:37

1:10:37

Credit Risk - Probability of Default, End-to-End Model Development | Beginner to Pro Level

0:01:11

0:01:11

Parâmetro de Perdas Esperadas Loss Given Default (#LGD).

0:20:55

0:20:55

International Basel IV-Channel, LGD Downturn Estimation, 05.10.2018

1:52:00

1:52:00

Credit Risk Modelling Introduction to PD LGD EAD Day04

0:40:51

0:40:51

IRB Approach_Probability of Default _SAS EM - 10

0:05:01

0:05:01

Calculating Expected Losses (EL) & loan loss provisioning under Basel with Excel example

0:23:26

0:23:26

Modeling Credit Risk - Part 2| Probability of Default | Loss Given Default | Expected Loss

1:47:52

1:47:52

Credit Risk Modelling Introduction to PD LGD EAD Variables Day05

0:14:48

0:14:48

Calculating LGD (Loss given default)

0:13:39

0:13:39

Survival Analysis (Part 1) - Advanced Credit Risk Management Course (Sample Video)

Комментарии