filmov

tv

The ULTIMATE Tax-Free Income Strategy: Whole Life Insurance

Показать описание

The ULTIMATE Tax-Free Income Strategy: Whole Life Insurance

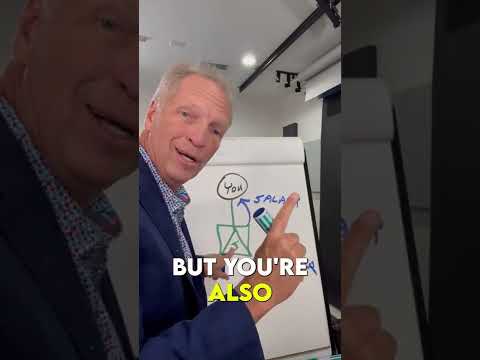

Whole life insurance, unlike term insurance, offers a lifetime coverage alongside an accumulating cash value component, which grows over time. This unique feature is what makes it an intriguing option for retirement planning. The video begins by demystifying the complex nature of whole life insurance policies, breaking down the terms, conditions, and benefits in a way that is accessible and understandable to both financial novices and seasoned investors.

The central thesis of the video is the strategic utilization of the cash value component of whole life insurance. We explain how policyholders can borrow against the cash value of their insurance as a tax-free source of income during retirement. This method of generating income is particularly appealing because it does not directly impact one's Canada Pension Plan and Old Age Security benefits or result in additional tax liabilities. Furthermore, if managed wisely, the policy remains intact, continuing to provide the death benefit to beneficiaries.

To provide a comprehensive understanding, the video covers the intricacies of policy loans, including interest rates, repayment terms, and the effects of unpaid loans on the death benefit. It emphasizes the importance of policy management and how mismanagement could potentially erode the death benefit. Practical advice on how to balance withdrawals to maintain the policy's integrity while ensuring it serves as a reliable income source during retirement.

In addition to theoretical knowledge, the video showcases real-life case studies of individuals who have successfully integrated whole life insurance into their retirement planning. These examples offer tangible insights into the process and outcomes of leveraging life insurance for retirement income, highlighting both the challenges encountered and the strategies employed to overcome them.

In essence, "How to Generate Retirement Income Using Whole Life Insurance" is a must-watch for anyone interested in exploring innovative financial strategies for retirement. It provides valuable insights into how whole life insurance can be more than just a safety net for one's heirs but a dynamic tool in ensuring a financially secure and prosperous retirement.

𝗪𝗵𝘆 𝗬𝗼𝘂 𝗦𝗵𝗼𝘂𝗹𝗱 𝗪𝗮𝘁𝗰𝗵:

This video is not just for economists or financial experts; it’s for anyone concerned about their financial well-being in the coming years. If you're looking for ways to safeguard your investments, plan for retirement, or understand the economic indicators that could impact your future, this video is your go-to resource.

By the end of this discussion, you’ll have a clearer understanding of the driving forces behind rising interest rates, market volatility, CPP / OAS, Retirement planning and the tools you'll need for protecting your assets and ensuring a secure financial future.

Don't leave your financial future to chance. Equip yourself with the knowledge you need and consider getting professional advice to navigate these uncertain times. Subscribe for more insights and actionable tips.

Disclaimer: This video is for informational purposes only and should not be considered as financial advice.

➤ 𝐇𝐨𝐰 𝐈 𝐡𝐞𝐥𝐩 𝐌𝐲 𝐂𝐥𝐢𝐞𝐧𝐭𝐬 𝐀𝐜𝐡𝐢𝐞𝐯𝐞 𝐓𝐡𝐞𝐢𝐫 𝐆𝐨𝐚𝐥𝐬:

➤ Business Inquiries:

☎️ 1-866-623-8368

⚡ 𝗖𝗼𝗻𝗻𝗲𝗰𝘁 𝘄𝗶𝘁𝗵 𝗗𝗮𝘃𝗶𝗱 𝗔𝗮𝗿𝗼𝗻 𝗼𝗻 𝗦𝗼𝗰𝗶𝗮𝗹 𝗠𝗲𝗱𝗶𝗮

Toronto Mississauga Oakville Burlington Brampton Woodbridge Vaughan Richmond Hill Newmarket Thornhill NorthYork GTA Etobicoke Markham Aurora King City Ontario Manitoba British Columbia Alberta New Brunswick

#retirementplanning #wholelifeinsurance

Whole life insurance, unlike term insurance, offers a lifetime coverage alongside an accumulating cash value component, which grows over time. This unique feature is what makes it an intriguing option for retirement planning. The video begins by demystifying the complex nature of whole life insurance policies, breaking down the terms, conditions, and benefits in a way that is accessible and understandable to both financial novices and seasoned investors.

The central thesis of the video is the strategic utilization of the cash value component of whole life insurance. We explain how policyholders can borrow against the cash value of their insurance as a tax-free source of income during retirement. This method of generating income is particularly appealing because it does not directly impact one's Canada Pension Plan and Old Age Security benefits or result in additional tax liabilities. Furthermore, if managed wisely, the policy remains intact, continuing to provide the death benefit to beneficiaries.

To provide a comprehensive understanding, the video covers the intricacies of policy loans, including interest rates, repayment terms, and the effects of unpaid loans on the death benefit. It emphasizes the importance of policy management and how mismanagement could potentially erode the death benefit. Practical advice on how to balance withdrawals to maintain the policy's integrity while ensuring it serves as a reliable income source during retirement.

In addition to theoretical knowledge, the video showcases real-life case studies of individuals who have successfully integrated whole life insurance into their retirement planning. These examples offer tangible insights into the process and outcomes of leveraging life insurance for retirement income, highlighting both the challenges encountered and the strategies employed to overcome them.

In essence, "How to Generate Retirement Income Using Whole Life Insurance" is a must-watch for anyone interested in exploring innovative financial strategies for retirement. It provides valuable insights into how whole life insurance can be more than just a safety net for one's heirs but a dynamic tool in ensuring a financially secure and prosperous retirement.

𝗪𝗵𝘆 𝗬𝗼𝘂 𝗦𝗵𝗼𝘂𝗹𝗱 𝗪𝗮𝘁𝗰𝗵:

This video is not just for economists or financial experts; it’s for anyone concerned about their financial well-being in the coming years. If you're looking for ways to safeguard your investments, plan for retirement, or understand the economic indicators that could impact your future, this video is your go-to resource.

By the end of this discussion, you’ll have a clearer understanding of the driving forces behind rising interest rates, market volatility, CPP / OAS, Retirement planning and the tools you'll need for protecting your assets and ensuring a secure financial future.

Don't leave your financial future to chance. Equip yourself with the knowledge you need and consider getting professional advice to navigate these uncertain times. Subscribe for more insights and actionable tips.

Disclaimer: This video is for informational purposes only and should not be considered as financial advice.

➤ 𝐇𝐨𝐰 𝐈 𝐡𝐞𝐥𝐩 𝐌𝐲 𝐂𝐥𝐢𝐞𝐧𝐭𝐬 𝐀𝐜𝐡𝐢𝐞𝐯𝐞 𝐓𝐡𝐞𝐢𝐫 𝐆𝐨𝐚𝐥𝐬:

➤ Business Inquiries:

☎️ 1-866-623-8368

⚡ 𝗖𝗼𝗻𝗻𝗲𝗰𝘁 𝘄𝗶𝘁𝗵 𝗗𝗮𝘃𝗶𝗱 𝗔𝗮𝗿𝗼𝗻 𝗼𝗻 𝗦𝗼𝗰𝗶𝗮𝗹 𝗠𝗲𝗱𝗶𝗮

Toronto Mississauga Oakville Burlington Brampton Woodbridge Vaughan Richmond Hill Newmarket Thornhill NorthYork GTA Etobicoke Markham Aurora King City Ontario Manitoba British Columbia Alberta New Brunswick

#retirementplanning #wholelifeinsurance

0:06:21

0:06:21

The ULTIMATE Tax-Free Income Strategy: Whole Life Insurance

0:44:35

0:44:35

How Real Estate is the Ultimate Tax-Free Strategy - Robert Kiyosaki

0:11:56

0:11:56

Buy, Borrow, Die: The Ultimate Tax-Free Wealth Strategy!

0:16:22

0:16:22

Here’s How to Pay $0 Taxes on $100k Retirement Income

0:00:56

0:00:56

How the rich live tax free. Buy. Borrow. Die. #shorts

0:46:54

0:46:54

Make your Income Tax ZERO! | Ultimate Tax Saving Masterclass | LLA

0:32:14

0:32:14

Avoid Taxes with The Ultimate Tax Strategy Guide

0:08:31

0:08:31

How to generate £40,000 TAX-FREE RETIREMENT INCOME

0:02:34

0:02:34

Tax Time Made Easy A Beginner's Guide to Filing Federal Income Taxes

0:01:00

0:01:00

How to Lower Your Taxes as a High-Income Earner

0:25:04

0:25:04

The Ultimate Guide to Tax-Free Income in Retirement

0:00:35

0:00:35

The Best Tax-Free Retirement Strategy

0:01:26

0:01:26

The 'finance cheat code' - Ultimate Tax-Free Strategy for Small Business Owners

0:00:32

0:00:32

THE ONLY 3 ACCOUNTS YOU'LL EVER NEED

0:00:41

0:00:41

How To Avoid Paying Taxes...Legally

0:09:26

0:09:26

The Top 5 Ways to Reduce Taxes on W2 & Active Income

0:00:29

0:00:29

5 CRORE Income - par TAX kitna?! | Ankur Warikoo #shorts

0:00:40

0:00:40

Investing in Residential Real Estate: The Ultimate Tax-Free Monthly Income Strategy

0:00:40

0:00:40

Robert Kiyosaki: The Best Investment Strategy in the World 🔥📈 #money #investing #finance

0:01:00

0:01:00

Why Pensions are the Ultimate Tax-Free Investment Strategy! 💰📈 | #Podcast #SmartInvesting #Financial...

0:07:29

0:07:29

4 Income Sources NOT Taxed In Retirement - Tax Efficient Withdrawal Strategy

1:28:10

1:28:10

Ultimate Tax Avoidance Strategy: 'Buy, Borrow, Die' explained. The Perfect Portfolio Overv...

0:16:24

0:16:24

Ultimate tax saving guide 2024 | Calculating income tax | Tax-saving deductions and exemptions

0:00:50

0:00:50

How to pay yourself when you start an LLC taxed as an S-corp... 💸 Big tax savings tip! #shorts

Комментарии