filmov

tv

Options Payoffs and Profits & Losses (Calculations for CFA® and FRM® Exams)

Показать описание

AnalystPrep's Concept Capsules for CFA® and FRM® Exams

This series of video lessons is intended to review the main calculations required in your CFA and FRM exams.

*AnalystPrep is an Official GARP-Approved Exam Preparation Provider*

Options

The buyer of an option has the right but not the obligation to exercise the option. The maximum loss to the buyer is equal to the premium paid for the option. The potential gains are theoretically infinite. To the seller (writer), however, the maximum gain is limited to the premium received after writing the option. The potential loss is unlimited.

In an options contract, two parties transact simultaneously. The buyer of a call or a put option is the long position in the contract while the seller of the option, also known as the writer of the option, is the short position.

Long vs. Short

Here is it important to differentiate between the long and the short party in a contract. The buyer is always said to be long the option. This is quite easy to see for a call option.

However, for a put option, the long position in a put is betting that the underlying price will drop. As such, the long position in a put option is synonymous to being short the underlying.

Expiration

Exchange-traded stock options can either be American or European style. While European options can only be exercised at expiry, American options can be exercised at any point during the life of the option. The actual date of expiry is specified by the exchange.

Strike Prices

Тhe value of the stock directly controls the strike price. At the expiration date, the difference between the stock’s market price and the option’s strike price determines the payoff.

Moneyness

For Call Options:

▪ If the stock price exceeds the exercise price, the option is in-the-money (ITM).

▪ If the stock price is less than the exercise price, the option is out-of-the-money (OTM).

▪ If the current market price is equal to the strike price, the option is at-the-money (ATM).

For Put Options: Just the opposite

▪ If the stock price is less than exercise price, the option is in-the-money (ITM).

▪ If the stock price exceeds the exercise price, the option is out-of-the-money (OTM).

▪ If the current market price is equal to the strike price, the option is at-the-money (ATM).

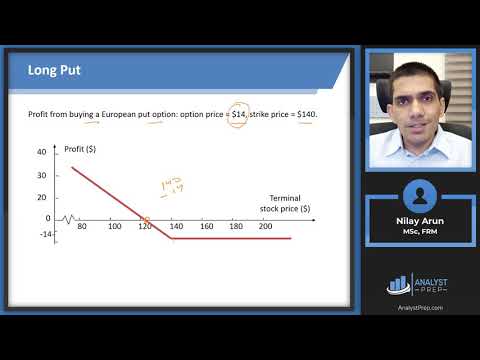

Intrinsic Value and Time Value

The intrinsic value of an option is the difference between the prevailing market price of the underlying and the strike price.

▪ Intrinsic value of a call option = max(0, St − X)

▪ Intrinsic value of a put option = max(0, X − St)

This series of video lessons is intended to review the main calculations required in your CFA and FRM exams.

*AnalystPrep is an Official GARP-Approved Exam Preparation Provider*

Options

The buyer of an option has the right but not the obligation to exercise the option. The maximum loss to the buyer is equal to the premium paid for the option. The potential gains are theoretically infinite. To the seller (writer), however, the maximum gain is limited to the premium received after writing the option. The potential loss is unlimited.

In an options contract, two parties transact simultaneously. The buyer of a call or a put option is the long position in the contract while the seller of the option, also known as the writer of the option, is the short position.

Long vs. Short

Here is it important to differentiate between the long and the short party in a contract. The buyer is always said to be long the option. This is quite easy to see for a call option.

However, for a put option, the long position in a put is betting that the underlying price will drop. As such, the long position in a put option is synonymous to being short the underlying.

Expiration

Exchange-traded stock options can either be American or European style. While European options can only be exercised at expiry, American options can be exercised at any point during the life of the option. The actual date of expiry is specified by the exchange.

Strike Prices

Тhe value of the stock directly controls the strike price. At the expiration date, the difference between the stock’s market price and the option’s strike price determines the payoff.

Moneyness

For Call Options:

▪ If the stock price exceeds the exercise price, the option is in-the-money (ITM).

▪ If the stock price is less than the exercise price, the option is out-of-the-money (OTM).

▪ If the current market price is equal to the strike price, the option is at-the-money (ATM).

For Put Options: Just the opposite

▪ If the stock price is less than exercise price, the option is in-the-money (ITM).

▪ If the stock price exceeds the exercise price, the option is out-of-the-money (OTM).

▪ If the current market price is equal to the strike price, the option is at-the-money (ATM).

Intrinsic Value and Time Value

The intrinsic value of an option is the difference between the prevailing market price of the underlying and the strike price.

▪ Intrinsic value of a call option = max(0, St − X)

▪ Intrinsic value of a put option = max(0, X − St)

0:22:07

0:22:07

Options Payoffs and Profits & Losses (Calculations for CFA® and FRM® Exams)

0:03:22

0:03:22

Call payoff diagram | Finance & Capital Markets | Khan Academy

0:09:29

0:09:29

Payoff Diagrams for Options | Call Options | Put Options | Options Long | Options Short

0:08:48

0:08:48

Call Options Explained: Understanding Short and Long Calls

0:22:59

0:22:59

Options - Call & Put Payoffs and Basic Strategies

0:07:31

0:07:31

Options Trading: Understanding Option Prices

0:03:24

0:03:24

Put payoff diagram | Finance & Capital Markets | Khan Academy

0:04:21

0:04:21

Calculating gains and losses on Call and Put option transactions

0:19:46

0:19:46

Options: Calls, Puts, and Payoffs

0:03:08

0:03:08

Call writer payoff diagram | Finance & Capital Markets | Khan Academy

0:21:03

0:21:03

Option Payoff and Profit Diagrams.mp4

0:07:30

0:07:30

Easily Understand Put/Call Payoffs!

0:07:48

0:07:48

Options Writer: Payoffs and Profits of a Writer

0:03:53

0:03:53

Long straddle | Finance & Capital Markets | Khan Academy

0:22:51

0:22:51

Commodity and derivative market |Solving Call Option :Buyer's Payoff Problem Sums | Part 1 | TY...

0:32:10

0:32:10

Options Payoffs and Profits & Losses

0:34:13

0:34:13

Working with Option Payoffs

0:04:07

0:04:07

Put writer payoff diagrams | Finance & Capital Markets | Khan Academy

0:10:16

0:10:16

Stock Options Explained

0:06:53

0:06:53

What is a Call Spread? Financial Options - Financial Derivatives

0:12:13

0:12:13

Put and Call Payoffs in Excel

0:03:52

0:03:52

Bull Call Spread | Investopedia

0:12:25

0:12:25

Intro to Options

0:13:45

0:13:45

Commodity and derivative market |Solving Put Option :Buyer's Payoff Problem Sums | Part 1 | TYB...

Комментарии