filmov

tv

How to Import Historical Data from Interactive Brokers Using Python: Quick Tutorial | Quantreo

Показать описание

This video shows you how to connect with TWS and extract historical data efficiently using the Python API. Whether you're new to data analysis or a seasoned trader, you'll find this guide helpful for integrating Interactive Brokers with Python.

Don't forget to subscribe, like, and leave a comment to stay updated with more Python tutorials and trading tips.

The video is about How to Import Historical Data from Interactive Brokers Using Python: Quick Tutorial but also tries to cover the following subjects:

Python API for IBKR

Historical data extraction

Interactive Brokers integration

How to Import Historical Data from Interactive Brokers Using Python: Quick Tutorial | Quantreo

✅ Subscribe To My Channel For More Videos:

✅ Important Links:

✅ Stay Connected With Me:

==============================

✅ Other Videos You Might Be Interested In Watching:

👉 Build Your First Python Trading Bot: Step-by-Step Tutorial for Beginners | Quantreo

👉 How to Trade Live with MetaTrader 5 Using Python - (Free Template Included) | Quantreo

👉 Profitable Algorithmic Trading: Easy Guide to Build Successful Strategies | Quantreo

👉 Build a Trading Bot in 1 Week: Complete Road Map Challenge | Quantreo

=============================

✅ About Quantreo:

Create your "Trading Strategies Factory" with the Alpha Quant Program ...

Are you struggling to code your trading strategy?

Are you struggling to backtest a strategy quickly and properly?

Are you struggling to verify the robustness of a trading strategy?

Are you struggling to convert you trading strategies into live trading bots on MT5?

Are you struggling to integrate Machine Learning in your trading strategies?

Are you looking for a premium Quant community?

IF YOU ANSWERED "YES" TO ONE OF THESE QUESTIONS, you should take a look of our Alpha Quant Program !

For collaboration and business inquiries, please use the contact information below:

=====================

#interactivebrokers #pythonapi #databars #historicaldata #pythoncoding #ibkr #twstutorial #dataintegration

Disclaimer: I am not authorized by any financial authority to give investment advice. This video is for educational purposes only. I disclaim all responsibility for any loss of capital on your part. Moreover, 78.18% of private investors lose money trading CFD. Use of the information and instructions contained in this work is at your own risk. If any code samples or other technologies, this work contains or describes are subject to open-source licenses or the intellectual property rights of others, it is your responsibility to ensure that your use thereof complies with such licenses and/or rights. This video is not intended as financial advice. Please consult a qualified professional if you require financial advice. Past performance is no indication of future performance.

Copyright Disclaimer: Under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship and research. Fair use is a use permitted by copyright statute that might otherwise be infringing. Non-profit, educational or personal use tips the balance in favor of fair use

© Quantreo

0:03:18

0:03:18

How to import Historical data in MetaTrader [FREE ONLINE APP]

0:03:16

0:03:16

How to import Historical data in EA Studio

0:03:08

0:03:08

How to import Historical data in FSB Pro

0:02:42

0:02:42

How to import historical data in OtoAccess® Database

0:02:45

0:02:45

How to import historical data to your new OtoAccess Database

0:03:09

0:03:09

MT4 Historical Data Export and Import in Excel | English Sub-Title |

0:04:25

0:04:25

RealtimeDataExpress :: How to Import Historical Data

0:05:54

0:05:54

How to Import Historical Data from Interactive Brokers Using Python: Quick Tutorial | Quantreo

0:05:06

0:05:06

MT4 Historical Data Export and Import in Excel

0:01:00

0:01:00

How to import bitmex bitcoin historical data to mt4?

0:01:27

0:01:27

FundsMaster 3 Tutorial - Import Historical Data

0:00:16

0:00:16

Import Historical Data API Collection file to Postman

0:08:01

0:08:01

No Official Klaviyo Integration? Here is How to Import Historical Data Into Klaviyo

0:07:14

0:07:14

How to Import Historical Stock Market Data form Yahoo Finance in R

0:01:42

0:01:42

Dynamically Import Historical Stock Data Directly into Google Sheets in Seconds

0:08:11

0:08:11

7a Import Historical Data

0:06:45

0:06:45

How to import free historical data into any trading platform

0:03:23

0:03:23

Import Basic Historical Data part 1

0:01:51

0:01:51

18. How do I import project and update historical data ?

0:02:08

0:02:08

Import historical data from Strava to Garmin Connect

0:08:47

0:08:47

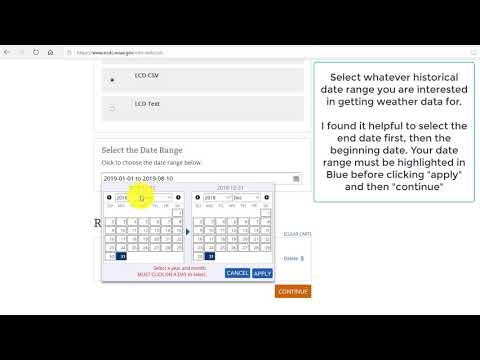

How to Import Historical Weather Data in Excel Deer Hunting Log Book

0:09:33

0:09:33

Import of the historical data into Customer Data Platform

0:00:48

0:00:48

Import Data Into Amibroker

0:09:07

0:09:07

How To Import Stock Historical Data From Yahoo Finance In Power BI With Python

Комментарии