filmov

tv

IFRS 16 Summary

Показать описание

Here's a summary of IFRS 16 for both lessees and lessors.

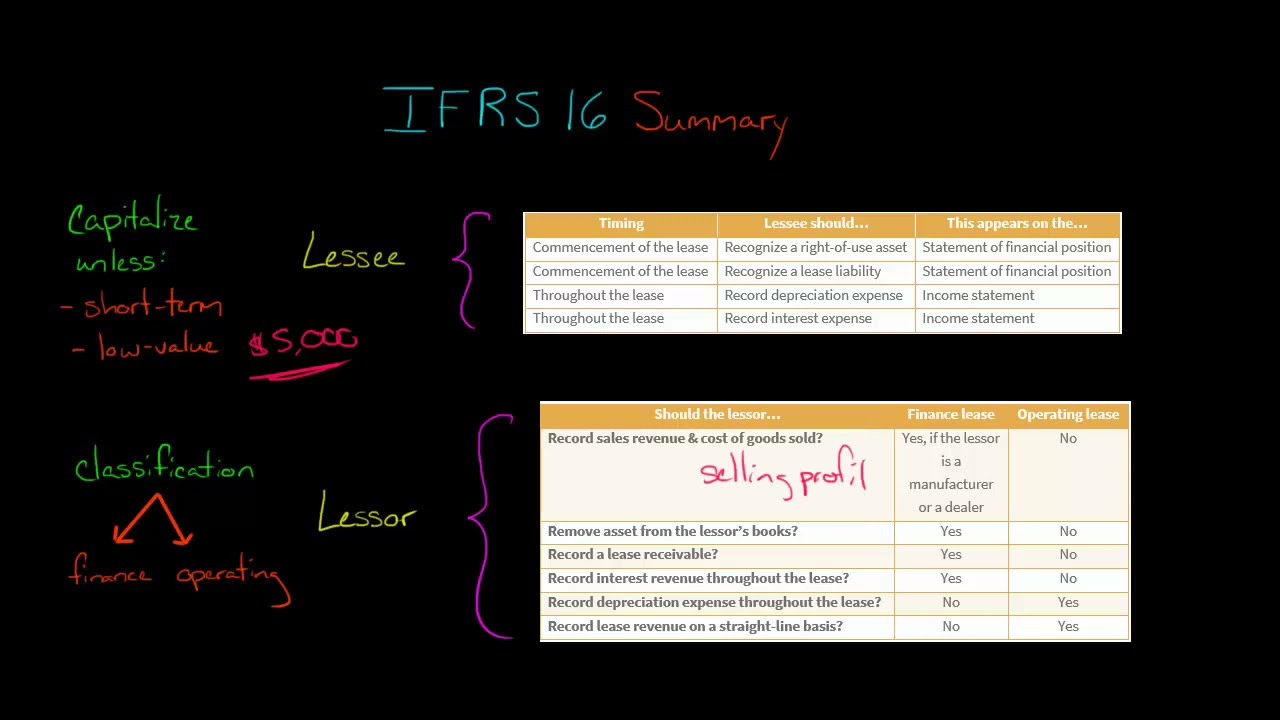

Lessees must capitalize all leases except for short-term leases (12 months or less) and leases of low-value assets (asset has a fair value of $5,000 or less at the beginning of the lease). Capitalization means the lessee must record a right-of-use asset and a lease liability on its statement of financial position at the commencement of the lease. The lessee then records depreciation expense (for the right-of-use asset) and interest expense (for the lease liability) throughout the lease term.

Lessors must first classify their lease as a finance lease or an operating lease, as this has a significant effect on the lessor's accounting. If the lease is a finance lease, the lessor must derecognize the asset from its statement of financial position and record a lease receivable upon commencement of the lease. (If the lessor is a manufacturer or a dealer, the lessor must also record sales revenue and cost of goods sold upon commencement of the lease.) The lessor then records interest revenue (for the lease receivable) throughout the lease term.

If the lessor has classified the lease as an operating lease, then the lessor should not remove the asset from its statement of financial position or record a lease receivable upon commencement of the lease. (Also, the lessor should not recognize sales revenue or cost of goods sold, even if it is a manufacturer or a dealer.) When it comes to the income statement, the lessor records depreciation expense (because the asset is still on the lessor's books) and records lease revenue on a straight-line basis throughout the lease term.

—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

Lessees must capitalize all leases except for short-term leases (12 months or less) and leases of low-value assets (asset has a fair value of $5,000 or less at the beginning of the lease). Capitalization means the lessee must record a right-of-use asset and a lease liability on its statement of financial position at the commencement of the lease. The lessee then records depreciation expense (for the right-of-use asset) and interest expense (for the lease liability) throughout the lease term.

Lessors must first classify their lease as a finance lease or an operating lease, as this has a significant effect on the lessor's accounting. If the lease is a finance lease, the lessor must derecognize the asset from its statement of financial position and record a lease receivable upon commencement of the lease. (If the lessor is a manufacturer or a dealer, the lessor must also record sales revenue and cost of goods sold upon commencement of the lease.) The lessor then records interest revenue (for the lease receivable) throughout the lease term.

If the lessor has classified the lease as an operating lease, then the lessor should not remove the asset from its statement of financial position or record a lease receivable upon commencement of the lease. (Also, the lessor should not recognize sales revenue or cost of goods sold, even if it is a manufacturer or a dealer.) When it comes to the income statement, the lessor records depreciation expense (because the asset is still on the lessor's books) and records lease revenue on a straight-line basis throughout the lease term.

—

Edspira is the creation of Michael McLaughlin, an award-winning professor who went from teenage homelessness to a PhD. Edspira’s mission is to make a high-quality business education freely available to the world.

—

SUBSCRIBE FOR A FREE 53-PAGE GUIDE TO THE FINANCIAL STATEMENTS, PLUS:

• A 23-PAGE GUIDE TO MANAGERIAL ACCOUNTING

• A 44-PAGE GUIDE TO U.S. TAXATION

• A 75-PAGE GUIDE TO FINANCIAL STATEMENT ANALYSIS

• MANY MORE FREE PDF GUIDES AND SPREADSHEETS

—

SUPPORT EDSPIRA ON PATREON

—

GET CERTIFIED IN FINANCIAL STATEMENT ANALYSIS, IFRS 16, AND ASSET-LIABILITY MANAGEMENT

—

LISTEN TO THE SCHEME PODCAST

—

GET TAX TIPS ON TIKTOK

—

ACCESS INDEX OF VIDEOS

—

CONNECT WITH EDSPIRA

—

CONNECT WITH MICHAEL

—

ABOUT EDSPIRA AND ITS CREATOR

0:10:48

0:10:48

IFRS 16 Leases summary - applies in 2025

0:02:52

0:02:52

The Fundamentals of IFRS 16

0:04:14

0:04:14

IFRS 16 Summary

0:13:31

0:13:31

ACCA IFRS 16, Leases Overview | What is IFRS 16 simple summary? | Use and Implementation of #ifrs16

0:13:08

0:13:08

IFRS 16: Leases - Summary (Sir Murtaza Quaid) - Part 1/3

0:08:06

0:08:06

Example: Lease accounting under IFRS 16

0:05:38

0:05:38

Quick Summary of IFRS 16 Leases | Why is it better than IAS 17?

1:02:31

1:02:31

Understanding IFRS 16 - Leases | Financial Reporting Explained

0:15:19

0:15:19

IFRS 16 Summary - IFRS 16 Leases || Financial Reporting Lectures (IFRS Summary Videos)

0:09:36

0:09:36

IFRS 16 Short Summary #ifrs16 #leases #acca #sbr

0:02:26

0:02:26

IFRS 16 | Leases

0:59:42

0:59:42

IFRS 16 academic webinar

0:36:42

0:36:42

IFRS 16: Definition of a lease

0:11:48

0:11:48

IFRS 16: Leases - Summary (Sir Murtaza Quaid) - Part 2/3

0:10:47

0:10:47

IAS 16 Property, Plant & Equipment Explained (applies in 2025) + FREE Compliance Checklist

0:40:24

0:40:24

IFRS-16-Leases-Complete Revision With Illustrations IN JUST 40 MINUTES

0:14:45

0:14:45

CAF 5 (FAR 2) - IFRS 16: Leases - Summary (Sir Murtaza Quaid) - Part 3/3

0:11:41

0:11:41

IAS 17 Leases - summary

0:29:58

0:29:58

IFRS 16 LEASES - ACCOUNTING FOR LEASES( PART 1 ).

0:11:43

0:11:43

IFRS 16 Leases - Summary

0:02:26

0:02:26

The fundamentals of IAS 16

0:11:48

0:11:48

IFRS 16 Leases - updated link in the description

0:05:21

0:05:21

IFRS 16 Leases - Introduction - CIMA F1 Financial Reporting

0:00:38

0:00:38

IFRS 16 Quick Summary #ifrs #ifrsaccounting #ifrs16 #finance #accounting

Комментарии