filmov

tv

🚀Velocity Banking: How to Pay Off Credit Card Debt Fast 🚀

Показать описание

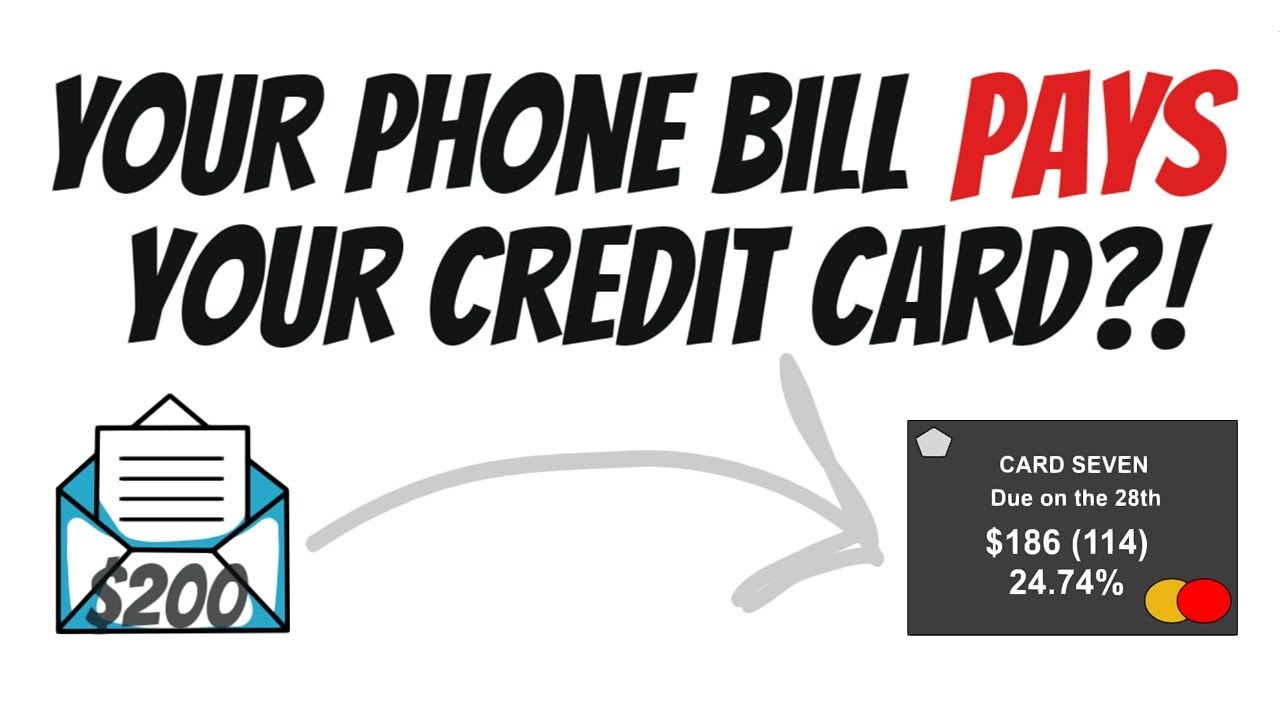

#howtopayoffcreditcarddebtfast Velocity Banking is THE strategy when you need to know how to pay off credit card debt fast! And when you're dealing with multiple credit cards, bill matching is a CRITICAL component of that strategy.

Thank you #ChristyVann @VanntasticFinances for explaining how #velocitybankingwithacreditcard works! I paid down $8,000 in credit card debt in 10 weeks!

Discover the power of Velocity Banking for rapid credit card debt payoff! Learn how to strategically match bills to credit card payments, prioritize your primary card, and leverage multiple cards to slash debt. Dive into this effective financial strategy step-by-step for faster debt elimination.

NOTE: I am not a financial advisor and I do not provide professional financial advice; the information presented on this channel is presented for information and edutainment purposes only. Following any words, actions, or advice in this video or on this channel as professional financial advice is not intended and is the responsibility of the viewer, not the video creator. This is my personal journey for getting out of credit card debt.

#velocitybanking, #Vanntasticfinance, #creditcarddebt, #velocitybankingwithacreditcard, #howtopayoffcreditcarddebtfast, #howtopayoffdebt #askmehowibudget, #creditcardinterest, #creditcardpayment, #velocitybankingstrategy, #creditcarddebt, #vanntastic, #creditutilization, #creditlimit

Thank you #ChristyVann @VanntasticFinances for explaining how #velocitybankingwithacreditcard works! I paid down $8,000 in credit card debt in 10 weeks!

Discover the power of Velocity Banking for rapid credit card debt payoff! Learn how to strategically match bills to credit card payments, prioritize your primary card, and leverage multiple cards to slash debt. Dive into this effective financial strategy step-by-step for faster debt elimination.

NOTE: I am not a financial advisor and I do not provide professional financial advice; the information presented on this channel is presented for information and edutainment purposes only. Following any words, actions, or advice in this video or on this channel as professional financial advice is not intended and is the responsibility of the viewer, not the video creator. This is my personal journey for getting out of credit card debt.

#velocitybanking, #Vanntasticfinance, #creditcarddebt, #velocitybankingwithacreditcard, #howtopayoffcreditcarddebtfast, #howtopayoffdebt #askmehowibudget, #creditcardinterest, #creditcardpayment, #velocitybankingstrategy, #creditcarddebt, #vanntastic, #creditutilization, #creditlimit

Velocity Banking Explained: A Step-by-Step Guide

Velocity Banking - The Truth about Paying off Your Mortgage Faster

WHAT IS VELOCITY BANKING? How to do #VelocityBanking with a credit card

Pay Off Debt with ZERO Cashflow: Don't cut expenses- use velocity banking!

Velocity Banking Basics In Elementary Terms

Velocity Banking: How Long Should You Wait To Pay Bills Out Of The HELOC?

🚀Velocity Banking: How to Pay Off Credit Card Debt Fast 🚀

How Do I Start Velocity Banking?

Part 6: Velocity Banking, Accelerated Banking, and Bill Matching 8-6-2024

What Can You Do When Your Credit Cards Are MAXED OUT? Velocity Banking!!🙌🏼🙌🏼🙌🏼

What Is Velocity Banking & How It's The FASTEST Way To Pay Off Debt!

How Can I Pay Off A Car Loan Quicker? Velocity Banking!

Is Velocity Banking Strategy a SCAM? Expert proves it doesn't work.

Using Velocity Banking to Payoff Multiple Credit Cards (No Line of Credit)

Pay Off Credit Cards FAST With This Simple Strategy! #velocitybanking

Making extra payments VS Velocity Banking with a credit card

Velocity Banking Pays Off $46,000 in One Year (All credit cards and car loan!)

Pay off any loan faster with credit cards - Velocity Banking Method

Velocity Banking: How To Turn Your Minimum Payment Into Cashflow and Pay $1200 With $600

Velocity Banking vs Sending In Extra Payment | Which Is Better?

Velocity Banking: ChatGPT Knows How It Can Eliminate Debt Faster Than Consolidation Loans

VELOCITY BANKING can PAY OFF your CREDIT CARD FAST!

Where Do I Start When I’m Paid Biweekly?? Velocity Banking Strategy

VELOCITY BANKING with a CREDIT CARD Explained #velocitybanking

Комментарии