filmov

tv

Covariance stationary processes

Показать описание

0:05:31

0:05:31

Covariance stationary processes

0:08:31

0:08:31

CFA® Level II Quant - Autoregressive (AR) Models: Mean reversion, Covariance Stationarity

0:08:52

0:08:52

0101 Covariance Stationarity

0:05:49

0:05:49

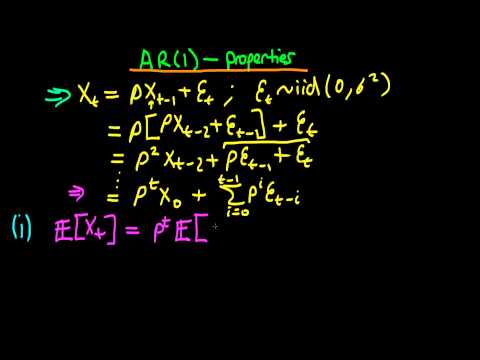

Autoregressive order 1 process - conditions for Stationary Covariance and Weak Dependence

0:10:02

0:10:02

Time Series Talk : Stationarity

0:04:08

0:04:08

Stationary series summary

0:07:11

0:07:11

Stata Time Series 2: Covariance Stationary Process (English version)

0:04:37

0:04:37

Conditions for stationary and weakly dependent series

0:03:49

0:03:49

Autoregressive order 1 process - conditions for stationary in mean

0:13:51

0:13:51

Derivatives of stochastic process, Jacobian/Hessian of covariance: stationary case (2)

0:06:35

0:06:35

On Autocovariances and Weak Stationarity

0:55:02

0:55:02

Times-series Analysis (2021 Level II CFA® Exam – Reading 6)

0:13:54

0:13:54

**Derivatives of stochastic process via Jacobian/Hessian of covariance: stationary case [moved]

![[Time Series] Weak](https://i.ytimg.com/vi/j6dmZqI0Bpw/hqdefault.jpg) 0:08:20

0:08:20

[Time Series] Weak Stationarity

0:25:25

0:25:25

stationarity in time series analysis #strictly stationary or weakly stationary#CS2

0:07:34

0:07:34

Weak Stationarity vs Strong Stationarity

0:11:38

0:11:38

Yule Walker Equation & Covariance of AR (2)

0:07:47

0:07:47

Covariance Clearly Explained!

0:11:32

0:11:32

Stationary Process | Strict Stationarity & Weak Stationarity || Time Series

0:08:02

0:08:02

Variance in AR2 Process

0:04:11

0:04:11

Variance stationary processes

0:09:22

0:09:22

Stationarity in Time Series

0:20:52

0:20:52

6.2 Random Processes: Joint Distribution, Independence, and Stationarity

0:23:38

0:23:38

Auto Covariance computation for Time Series

Комментарии