filmov

tv

How Long Until Your Roth Conversion Actually Pays Off in Retirement?

Показать описание

WORK WITH ME👇🏼

✅ See how we can help you get more out of early retirement

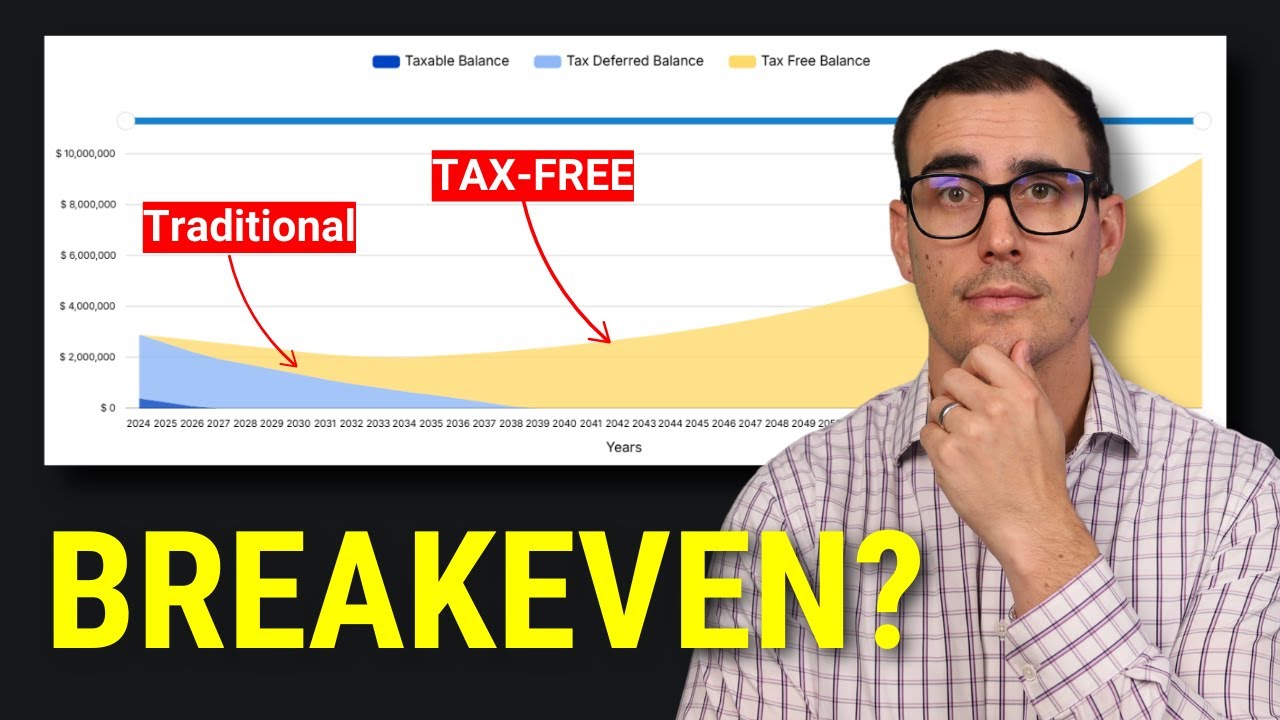

In the video, I explain when the best time to take a Roth conversion and other factors to look for before you decide how much to convert.

⚠️ "DISCLAIMER:⚠️

All content is not to be received as financial advice and each individual should consult with their dedicated financial planner, tax preparer, estate attorney, etc. before making any financial decisions.

All contents provided by This Channel is meant for EDUCATIONAL AND ENTERTAINMENT PURPOSE only.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you.

⚠️ "Scammer" Warning ➡ PLEASE READ! ⚠️ Be careful of scammers. In the comments section, I will NEVER ask you to contact me, offer any investment products, recommend a stock broker, or anything similar. Some scam bot commenters 'ask' for investment help, and later, other comment bots reply with "how great X idea/investment/person is" in the replies. These are scam threads. Do not fall for them

0:00 - Introduction

1:21 - Why even Consider a Roth Conversion?

3:26 - The Wrong way to view Roth Conversions

8:05 - When Can a Roth Conversion Payoff Sooner

10:00 - The Right way to view Roth Conversions

10:55 - Outro

✅ See how we can help you get more out of early retirement

In the video, I explain when the best time to take a Roth conversion and other factors to look for before you decide how much to convert.

⚠️ "DISCLAIMER:⚠️

All content is not to be received as financial advice and each individual should consult with their dedicated financial planner, tax preparer, estate attorney, etc. before making any financial decisions.

All contents provided by This Channel is meant for EDUCATIONAL AND ENTERTAINMENT PURPOSE only.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you.

⚠️ "Scammer" Warning ➡ PLEASE READ! ⚠️ Be careful of scammers. In the comments section, I will NEVER ask you to contact me, offer any investment products, recommend a stock broker, or anything similar. Some scam bot commenters 'ask' for investment help, and later, other comment bots reply with "how great X idea/investment/person is" in the replies. These are scam threads. Do not fall for them

0:00 - Introduction

1:21 - Why even Consider a Roth Conversion?

3:26 - The Wrong way to view Roth Conversions

8:05 - When Can a Roth Conversion Payoff Sooner

10:00 - The Right way to view Roth Conversions

10:55 - Outro

0:09:40

0:09:40

How Long Until Your Roth Conversion Pays Off? You might be surprised.

0:11:27

0:11:27

How Long Until Your Roth Conversion Actually Pays Off in Retirement?

0:03:28

0:03:28

Maxing Out Roth IRA Contributions for 6 Years Straight Has Earned Me this Much

0:11:44

0:11:44

The $65,000 Roth IRA Mistake To Avoid

0:00:41

0:00:41

My Biggest Roth IRA Mistake I Made

0:05:15

0:05:15

Roth IRA Withdrawal Rules

0:11:47

0:11:47

6 Reasons NOT to Convert to a Roth

0:09:49

0:09:49

Roth IRA Explained Simply for Beginners

0:00:16

0:00:16

Understanding ROTH IRA income Rules and Limits See where you Stand #SHORTS #IRA #ROTH IRA #Taxes

0:04:40

0:04:40

IRA Explained In Less Than 5 Minutes | Simply Explained

0:14:50

0:14:50

Watch This Before Roth Converting in 2024…trust me.

0:10:36

0:10:36

What Happens If You Max Your Roth IRA Every Year

0:04:46

0:04:46

NEW 2024 Roth IRA Income Rules & Limits You Need to Know

0:21:20

0:21:20

How Long to $1M with just a Roth IRA (Calculator Showdown)

0:08:40

0:08:40

You Need To Know This BEFORE Opening A Roth IRA

0:05:35

0:05:35

Should I Convert My Retirement To Roth?

0:03:36

0:03:36

At What Age does a Roth IRA not Make Sense?

0:10:49

0:10:49

Here’s Exactly How Much You Should Convert to Your Roth IRA to fill up the 22% Tax Bracket

0:00:51

0:00:51

DO NOT MAKE THIS ROTH IRA MISTAKE #investing #money #retirement #cash #rothira

0:11:38

0:11:38

When Is The Best Time To Max Out Your Roth???

0:12:20

0:12:20

Roth IRA Calculator by Age | How to Build Roth IRA to $1 Million

0:06:06

0:06:06

What Would Happen If You Maxed Out Your Roth IRA By Age?! (These Results Will Amaze You!)

0:10:11

0:10:11

When Should You Contribute To A Roth IRA?

0:15:36

0:15:36

FINANCIAL ADVISOR Explains: Retirement Plans for Beginners (401k, IRA, Roth 401k/IRA, 403b) 2024

Комментарии