filmov

tv

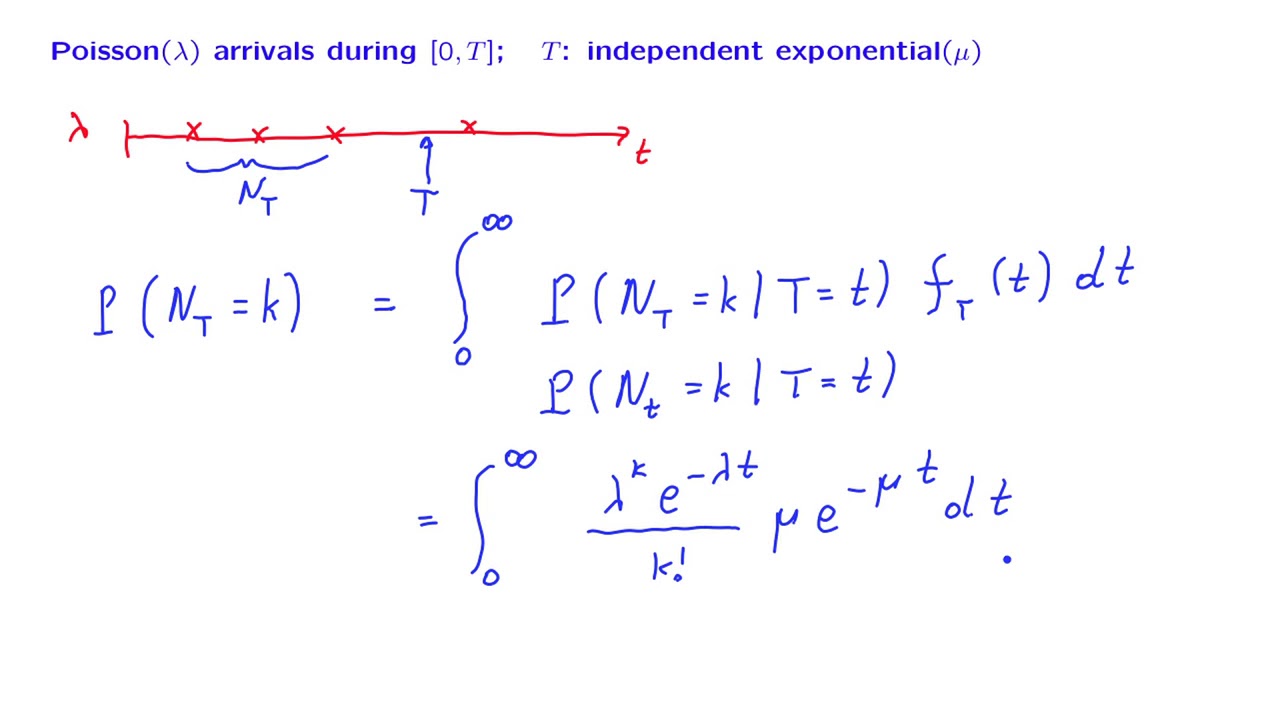

S23.2 Poisson Arrivals During an Exponential Interval

Показать описание

MIT RES.6-012 Introduction to Probability, Spring 2018

Instructor: John Tsitsiklis

License: Creative Commons BY-NC-SA

Instructor: John Tsitsiklis

License: Creative Commons BY-NC-SA

0:09:37

0:09:37

S23.2 Poisson Arrivals During an Exponential Interval

0:04:36

0:04:36

L23.8 Random Incidence in a Non-Poisson Process

0:01:18

0:01:18

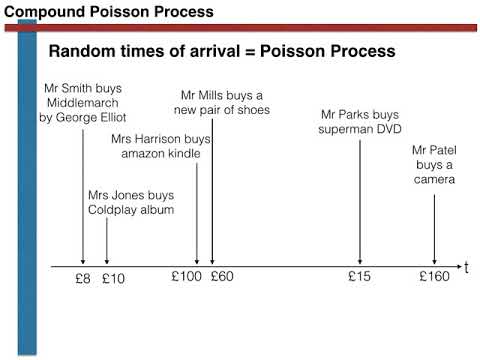

Simulating the compound poisson process

0:05:07

0:05:07

L22.2 Definition of the Poisson Process

0:04:03

0:04:03

L23.2 The Sum of Independent Poisson Random Variables

0:28:36

0:28:36

Pillai 'Poisson Processes and Coupon Collecting'

0:26:22

0:26:22

Pillai: Poisson Arrivals and Departures

0:09:48

0:09:48

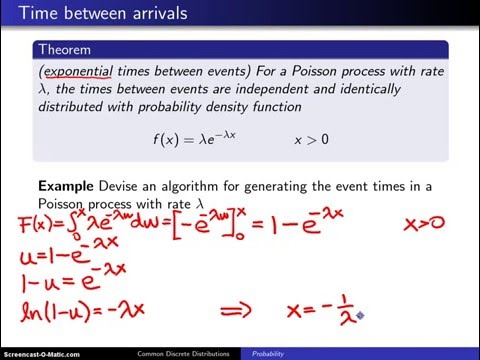

Poisson process time between arrivals

0:08:22

0:08:22

L23.3 Merging Independent Poisson Processes

0:06:59

0:06:59

Introduction to Poisson Process - Examples

0:09:09

0:09:09

L23.7 Random Incidence in the Poisson Process

0:25:21

0:25:21

Pillai: Next Waiting Time Inference for Random Poisson Arrivals

0:09:44

0:09:44

Probability Pillai 'Poisson Processes - Inter-arrival Distributions'

0:35:43

0:35:43

2 Poisson Processes

0:09:21

0:09:21

SP7 | Poisson Process | Exponential distribution | Stochastic Processes | Mannan | Arrival

0:09:45

0:09:45

Lecture 10.2: r. Waiting times, the exponential distribution — [Probability | Santosh S. Venkatesh]...

0:11:00

0:11:00

Pillai: Random Selection of Poisson Arrivals

0:12:00

0:12:00

Random Processes - 10 - Poisson Process Properties (Part 2)

0:10:02

0:10:02

SOR1020: The poisson process

0:32:19

0:32:19

13-02. Poisson processes - Poisson processes and the exponential distribution.

0:08:01

0:08:01

Evaluating a Non-Homogeneous Poisson Process | MAS 1 Fall 2018 Q2

0:09:08

0:09:08

43 Calculating the mean in Inverse Poisson Distribution questions

0:09:31

0:09:31

Pillai: Distribution of Departures Between Inter-Arrivals

0:21:42

0:21:42

Exponential + Poisson = Geometric Distribution!

Комментарии