filmov

tv

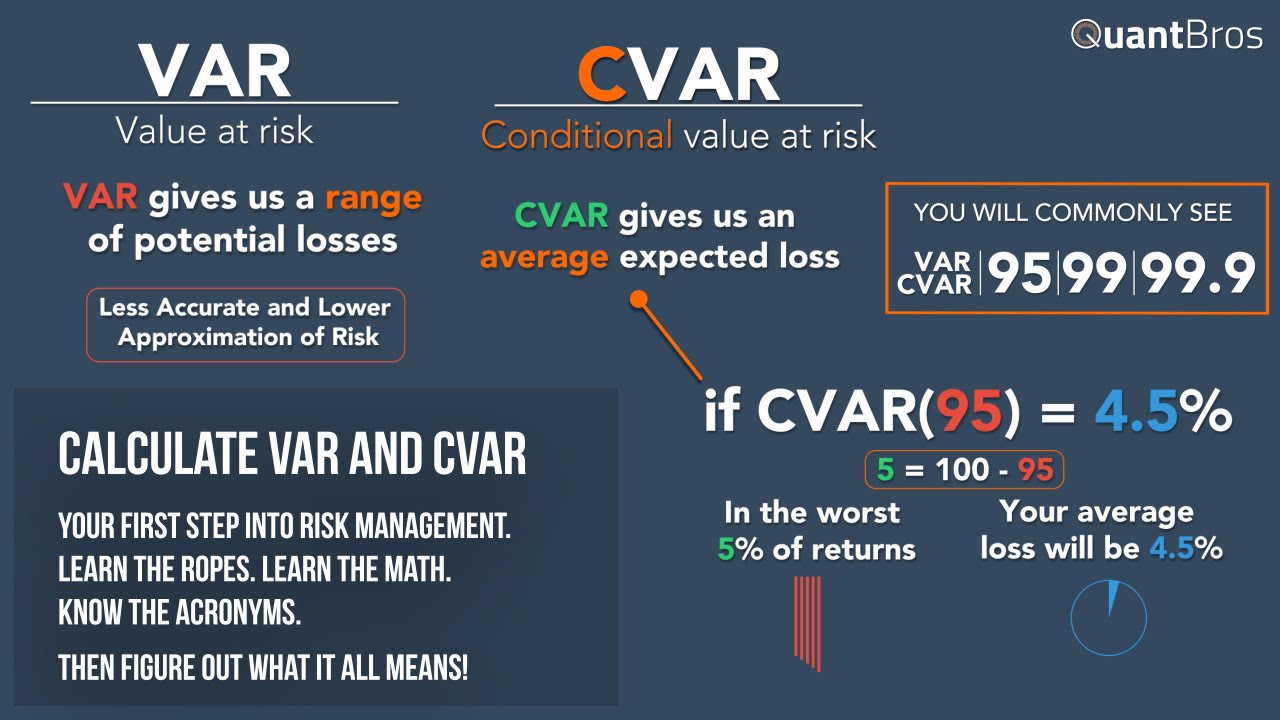

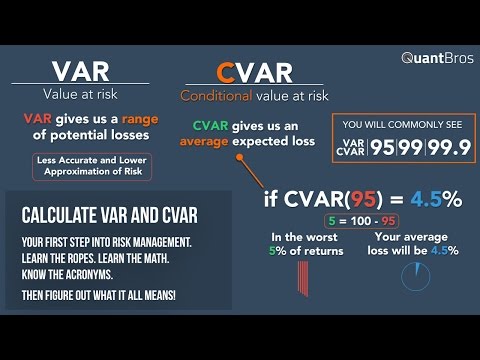

Calculating VAR and CVAR in Excel in Under 9 Minutes

Показать описание

Learn how to calculate VAR and CVAR in Excel. We'll also teach you the difference between VAR and CVAR.

Not enough for you? Want to learn more R? Our friends over at DataCamp will whip you into shape real quick if you need help:

Or if you're more of a Python guy, we have an intro to finance for Python course live on DataCamp right now:

Not enough for you? Want to learn more R? Our friends over at DataCamp will whip you into shape real quick if you need help:

Or if you're more of a Python guy, we have an intro to finance for Python course live on DataCamp right now:

0:09:02

0:09:02

Calculating VAR and CVAR in Excel in Under 9 Minutes

0:11:52

0:11:52

Expected Shortfall & Conditional Value at Risk (CVaR) Explained

0:05:09

0:05:09

Value at Risk Explained in 5 Minutes

0:14:53

0:14:53

Value at Risk (VaR) Explained!

0:11:04

0:11:04

Historical Value-at-Risk (VaR) and Conditional VaR (CVaR) in Excel

0:09:36

0:09:36

Conditional Value-at-Risk (Expected shortfall) - measuring expected extreme loss (Excel) (SUB)

0:05:03

0:05:03

Parametric VaR and CVaR (Gaussian/Normal Distribution) in Excel

0:10:26

0:10:26

Monte Carlo Simulation with value at risk (VaR) and conditional value at risk (CVaR) in Python

0:18:37

0:18:37

1000% Back Test Return On a Trading Bot ... Should I Quit My Job?

0:07:54

0:07:54

VaR (Value at Risk) and CVaR (Conditional Value at Risk) Explained in Graphics

0:13:09

0:13:09

Historical VAR Calculation in Excel | FRM & CFA Preparation

0:15:04

0:15:04

Parametric VaR and CVaR with Python

0:10:13

0:10:13

Monte Carlo Method: Value at Risk (VaR) In Excel

0:05:38

0:05:38

Conditional Value at Risk (CVaR) Portfolio Optimization

0:08:11

0:08:11

Cornish-Fisher VaR and CVaR in Excel

0:05:55

0:05:55

Value at Risk (VaR) Explained in 5 minutes

0:08:43

0:08:43

How do you calculate value at risk? Two ways of calculating VaR

0:02:26

0:02:26

What Is Conditional Value at Risk (CVaR)?

0:05:01

0:05:01

Historical Method: Value at Risk (VaR) In Excel

0:12:53

0:12:53

Value at Risk (VAR) | Risk Management | CA Final SFM

0:08:09

0:08:09

VaR for a multi-asset portfolio using variance covariance matrix

0:25:36

0:25:36

Portfolio & Single Stock VAR and CVAR in R

0:06:43

0:06:43

Conditional Value at Risk and Stress Testing in Financial Risk Management

0:06:25

0:06:25

What is Value at Risk? VaR and Risk Management

Комментарии