filmov

tv

Все публикации

0:11:16

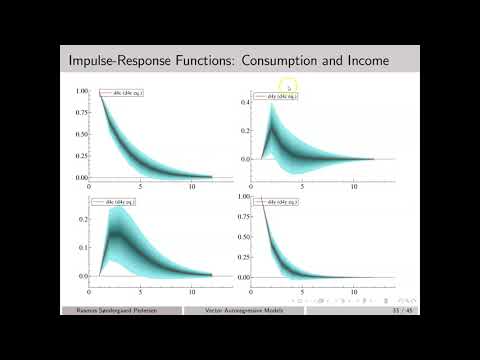

VAR Models: Impulse-Responses and Structural VAR Models

0:09:54

Estimation and Asymptotic Inference in Vector Autoregressive (VAR) Models

0:09:51

Stationarity Conditions for AR(2) Processes

0:07:16

Computation of news impact curve

0:16:50

GMM Estimation of Consumption CAPM

0:08:46

On exporting estimation results from PcGive (OxMetrics) to LaTeX.

0:17:16

An Introduction to Multivariate GARCH

0:16:47

An empirical illustration of the co-integrated VAR model

0:17:39

The Augmented Dickey-Fuller Test with Deterministic Terms

0:10:17

Efficient GMM Estimation

0:06:50

GMM Estimation and the Properties of the GMM Estimator

0:07:50

Introduction to GMM

0:08:22

Estimation of GARCH Models in OxMetrics

0:07:27

Maximum Likelihood Estimation of the MA(1) Model

0:07:44

OLS Estimation of the AR(1) Model

0:10:10

Maximum Likelihood Estimation of the AR(1) Model

0:11:16

0:11:16

0:09:54

0:09:54

0:09:51

0:09:51

0:07:16

0:07:16

0:16:50

0:16:50

0:08:46

0:08:46

0:17:16

0:17:16

0:16:47

0:16:47

0:17:39

0:17:39

0:10:17

0:10:17

0:06:50

0:06:50

0:07:50

0:07:50

0:08:22

0:08:22

0:07:27

0:07:27

0:07:44

0:07:44

0:10:10

0:10:10