filmov

tv

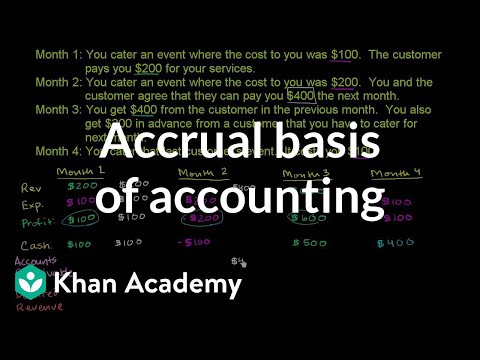

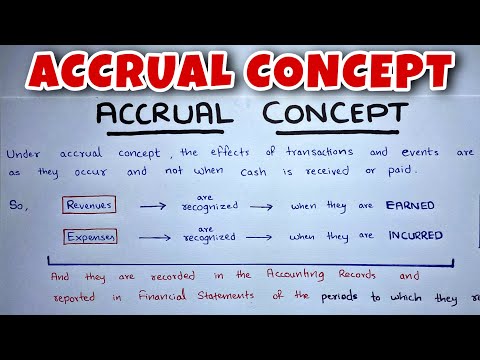

The Accrual basis of accounting and the reasons for adjusting entries.

Показать описание

CHAPTER

3

Adjusting the Accounts

Overview

In Chapter 1, you learned a neat little formula: Net income 5 Revenues 2

Expenses. In Chapter 2, you learned some rules for recording revenue and expense transactions. Guess

what? Things are not really that nice and neat. In fact, it is often diffi cult for companies to determine

in what time period they should report some revenues and expenses. In other words, in measuring net

income, timing is everything.

Learning Objectives 1st

Explain the accrual basis of accounting

and the reasons for adjusting entries

Topic involved

Fiscal and Calendar Years

Accrual- versus Cash-Basis Accounting

Recognizing Revenues and Expenses

The Need for Adjusting Entries

Types of Adjusting Entries

3

Adjusting the Accounts

Overview

In Chapter 1, you learned a neat little formula: Net income 5 Revenues 2

Expenses. In Chapter 2, you learned some rules for recording revenue and expense transactions. Guess

what? Things are not really that nice and neat. In fact, it is often diffi cult for companies to determine

in what time period they should report some revenues and expenses. In other words, in measuring net

income, timing is everything.

Learning Objectives 1st

Explain the accrual basis of accounting

and the reasons for adjusting entries

Topic involved

Fiscal and Calendar Years

Accrual- versus Cash-Basis Accounting

Recognizing Revenues and Expenses

The Need for Adjusting Entries

Types of Adjusting Entries

0:07:06

0:07:06

0:11:00

0:11:00

0:04:51

0:04:51

0:06:26

0:06:26

0:09:00

0:09:00

0:02:09

0:02:09

0:03:29

0:03:29

0:00:39

0:00:39

0:16:00

0:16:00

0:09:57

0:09:57

0:01:00

0:01:00

0:01:00

0:01:00

0:03:09

0:03:09

0:53:42

0:53:42

0:12:28

0:12:28

0:05:33

0:05:33

0:09:02

0:09:02

0:00:40

0:00:40

0:16:16

0:16:16

0:03:05

0:03:05

0:20:24

0:20:24

0:01:01

0:01:01

0:00:15

0:00:15

0:02:57

0:02:57