filmov

tv

Accounting Cycle

Показать описание

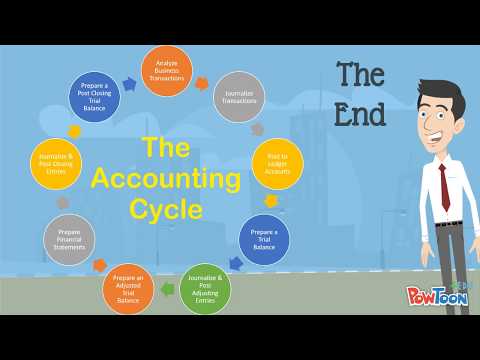

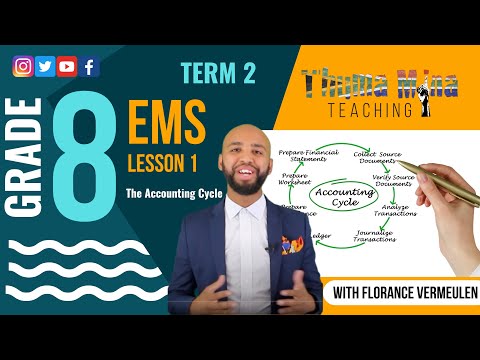

The Accounting Cycle is the term used to depict the collective process of recording transactions and processing them through the accounting system.

The purpose of the Accounting cycle is to reach the final stages of closing the books & releasing the entity’s financial statements. This process is perpetual, whereby it is completed at the end of the Accounting period and restarts at the beginning of the new period.

The seven stages of the Accounting Cycle are as follows:

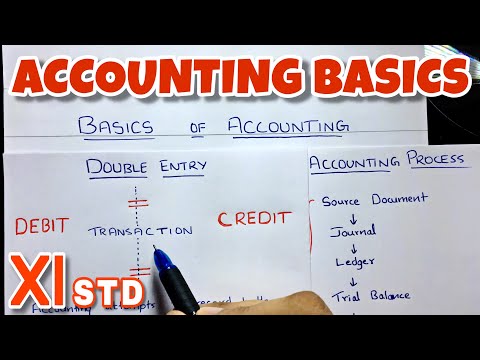

1- Source Documents / Transactions – Financial Transactions start the process, whereby data is collected and analyzed from source documents. These documents include such things as invoices, receipts, bank account documents (i.e statements & bank advices), etc that reflect transactions & events that have taken place related to an entity. These transactions can be for the sale of goods or services, payments to suppliers, employees, loans, the purchase or sale of assets, or even capital that is injected or taken out of the entity.

2- Journal Entries – Transactions are recorded in the appropriate journals related to the transactions in a chronological order. Sales transactions are reordered in the Sales Journal, Stock purchases transactions are recorded in the Purchases Journal, all Cash transactions are either recorded in the Cash Payments or Cash Receipts Journal, whilst the General journal is used for all other transactions that are not recorded in any of the journals above, such as adjustments of accounts.

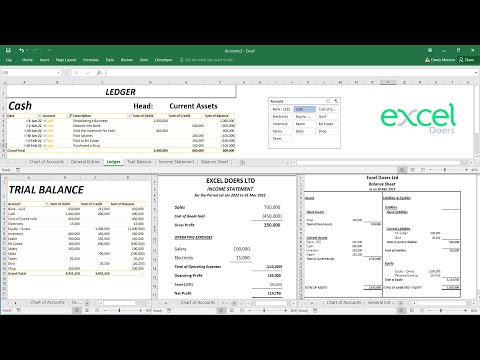

3- Posting / Ledger – The transactions are posted to the accounting Ledgers that they impact, whereby these accounts form part of the General Ledger. Each transaction will impact two accounts; one as a Debit & one as a Credit, depending on the actual transaction.

4- Trial Balance – Depending when you close your Accounting Period, you will need to run a Trial Balance report, making sure that all your Debit accounts equal all your Credit accounts. From the Trial Balance, you will be able to see the current balances of all your accounts.

5- Adjustments – Adjusting entries are accounting journal entries that reflect an entity's accounting records to the accrual basis of accounting. Prepayment & Accrual entries are processed for the related Revenues and Expenses that follow the Accrual Accounting Concept.

6- Closing Accounts & Stock Valuation – Trading entities will need to perform physical stock checks to make sure that their books reflect the correct actual stock position. Any discrepancies will need to be adjusted in the books before closure. All Revenue & Expense accounts are closed off to the Profit & Loss Summary account once all the accounts have been seen as being accurate. The net result of the P&L summary will equal the net profit or loss that the business incurred during the period, whereby it is transferred over to the Retained Earnings account.

7- Financial Statements – once the books have been closed, the Financial Statements are generated and released to internal managers. These include the Profit & Loss (or Income Statement) and Balance Sheet.

Depending on the size and structure of the Accounts department, you may have only one or many more people involved in the Accounting Cycle.

As they say – “Garbage in Garbage Out”, so make sure your accounting professionals complete the Accounting Cycle with care so that the end result (Financial Statements) is a true reflection of the financial performance of your entity.

Follow us on our social media channels:

The purpose of the Accounting cycle is to reach the final stages of closing the books & releasing the entity’s financial statements. This process is perpetual, whereby it is completed at the end of the Accounting period and restarts at the beginning of the new period.

The seven stages of the Accounting Cycle are as follows:

1- Source Documents / Transactions – Financial Transactions start the process, whereby data is collected and analyzed from source documents. These documents include such things as invoices, receipts, bank account documents (i.e statements & bank advices), etc that reflect transactions & events that have taken place related to an entity. These transactions can be for the sale of goods or services, payments to suppliers, employees, loans, the purchase or sale of assets, or even capital that is injected or taken out of the entity.

2- Journal Entries – Transactions are recorded in the appropriate journals related to the transactions in a chronological order. Sales transactions are reordered in the Sales Journal, Stock purchases transactions are recorded in the Purchases Journal, all Cash transactions are either recorded in the Cash Payments or Cash Receipts Journal, whilst the General journal is used for all other transactions that are not recorded in any of the journals above, such as adjustments of accounts.

3- Posting / Ledger – The transactions are posted to the accounting Ledgers that they impact, whereby these accounts form part of the General Ledger. Each transaction will impact two accounts; one as a Debit & one as a Credit, depending on the actual transaction.

4- Trial Balance – Depending when you close your Accounting Period, you will need to run a Trial Balance report, making sure that all your Debit accounts equal all your Credit accounts. From the Trial Balance, you will be able to see the current balances of all your accounts.

5- Adjustments – Adjusting entries are accounting journal entries that reflect an entity's accounting records to the accrual basis of accounting. Prepayment & Accrual entries are processed for the related Revenues and Expenses that follow the Accrual Accounting Concept.

6- Closing Accounts & Stock Valuation – Trading entities will need to perform physical stock checks to make sure that their books reflect the correct actual stock position. Any discrepancies will need to be adjusted in the books before closure. All Revenue & Expense accounts are closed off to the Profit & Loss Summary account once all the accounts have been seen as being accurate. The net result of the P&L summary will equal the net profit or loss that the business incurred during the period, whereby it is transferred over to the Retained Earnings account.

7- Financial Statements – once the books have been closed, the Financial Statements are generated and released to internal managers. These include the Profit & Loss (or Income Statement) and Balance Sheet.

Depending on the size and structure of the Accounts department, you may have only one or many more people involved in the Accounting Cycle.

As they say – “Garbage in Garbage Out”, so make sure your accounting professionals complete the Accounting Cycle with care so that the end result (Financial Statements) is a true reflection of the financial performance of your entity.

Follow us on our social media channels:

0:07:04

0:07:04

0:12:39

0:12:39

0:01:22

0:01:22

0:14:13

0:14:13

0:10:30

0:10:30

0:12:58

0:12:58

0:09:46

0:09:46

0:27:58

0:27:58

0:00:14

0:00:14

4:50:59

4:50:59

0:13:59

0:13:59

0:05:29

0:05:29

1:03:43

1:03:43

10:01:51

10:01:51

0:03:25

0:03:25

0:30:02

0:30:02

![[Financial Accounting]: Chapter](https://i.ytimg.com/vi/iIn2j52b_BI/hqdefault.jpg) 0:24:10

0:24:10

0:05:02

0:05:02

0:09:45

0:09:45

0:27:46

0:27:46

0:33:04

0:33:04

0:03:54

0:03:54

0:31:30

0:31:30

0:04:16

0:04:16